LVMH Moët Hennessy — Louis Vuitton Explained

Key Ideas

- LVMH has demonstrated extraordinary leadership and market strategy over years, along with healthy financials and growth opportunities, it led to be a great potential investment

- LVMH has conducted over 50 M&As and the House of Brands conglomerate business model has made phenononial effect in the fashion history

- In the future, LVMH might somehow have to somehow offset the problems with counterfeit and geographic expansions. Also they might have to embrace the rise of sustainability and diversity within the social context.

Introduction

LVMH — Moet Hennessy Louis Vuitton, a global luxury-leading conglomerate corporation which includes over 70 various top-tier designer fashion/beauty brands as subsidaries including Louis Vuitton, Christian Dior, Givenchy, Celine, Sephora etc. The Paris fashion group is operating under a very niche market at the top class retail chain, with his the only one and the biggest competitor — The Kerri Group, which includes Balenciaga, Gucci, Bottega Veneta, Puma etc.

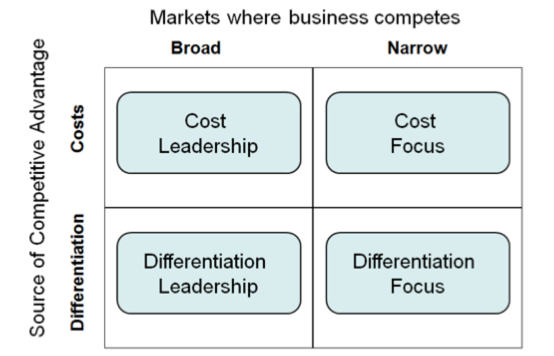

The business model of luxury brands is generally somehow differs from the regular consumers good. Apart from most business models, LVMH doesn’t rely on PP&E to generate sales but it really takes an extraordinary marketing strategy to position itself at an attractive space in the market. According to Porter Generic Strategy, LVMH is completing at a hybrid strategic competitions at differentiation leadership and differentiation focus. They advocate to insert the elegance image into their brands in the meantime they constantly innovate it’s products/services/distributional channels including sustainability integration, celebrities collaboration, environmental impact etc.

Strategy

The core competencies of LVMH along with other fashion brands are potential leadership, uniqueness of brands and products and distribution channels. Completing within this niche space they would definitely want to create a great image among investors and consumers as their competitive advantage, but on the other hand, they would still need to be able to create great designs to gather consumers together.

To execute this, Merger & Acquisition has played a significant role. Normally, M&A was meant to provide synergies where companies are vertically integrate their operations in order to cut cost and generate additional revenue by integrating their existing markets. For tech companies, the acquirer might want it’s potential of development and maybe intelligential properties like patents. For LVMH, they horizontally acquired companies within the landscape because they can share the distribution channels to certain extent and extract valuable human capital from the targets.

The dynamic capability of an organization to construct new consumer trend and innovations is crucial and LVMH has created these 5 branches on top of each subsidiary designer brand: Strategic and Financials, Talent Management, Creativity and Culture, Adaptability, and Responsiveness and Diversification. These branches enable the companies to better position itself within the marketplace and makes every brand of LVMH unique from each other.

Ultimately LVMH would strive to create value for the customer, though the products are expensive. Customer would look at the product as they are buying into their own dreams.

Past

In 1987, Moet Hennessy, the leading manufacturer of high-end champagne and cognac merged with Louis Vuitton with in a $4 billion deal. Which marked one of the biggest and the beginning conglomerate deals within the fashion space. Afterwards they had made different acquisitions following from Sephora (1997), beauty lines such as Hard Candy, Make Up For Ever (1999) and conducted partnerships within fashion retailers.

All Major M&A within the luxurious industry are listed within the link: http://www.thefashionlaw.com/home/lvmh-a-timeline-behind-the-building-of-a-conglomerate

In early 2000s, LVMH has relocated its headquarter in New York, the United States. The house of brands business model has also become really common for all luxurious industry, the rise of the Kerri Group, Coach and Michael Kors etc. LVMH had maintained five categories among its brands, including (1) Fashion & Leather Goods, (2)Selective Retailing, (3) Perfumes & Cosmetics, (4) Wines & Spirits and (5)Watches & Jewelry. (Arranged from most sales to least sales)

Most people might think operating at the luxurious industry, their performance would greatly tied within the consumer spendings behaviour. In 2008 financial crisis, a lot of people went bankrupt because of their mortgage debt and investment loss, the entire economy shrinked and most businesses had recorded a poor performance within that fiscal year.

Instead, LVMH and Kering Group have recorded a year with 5–8% organic growth in spite of the crisis while middle-end apparel groups like GAP and Tommy Hilfenger have recorded a significant drop in sales and profits. The identified strong market beta luxurious company had actually outperformed investor’s expectations and it can be explained as first they have a different income matrix including margins and leverage, secondly the demand of their goods are as price-sensitive as companies like GAP. Last but not least as they are actually targeting a very niche market in the wealthy group. Therefore, a lot of external factors might not be able to affect these brands like the way they affect the common retail brands.

Now

Last April, they released their first quarter result as they have recorded double-digit growth compared to last year. They have developed sustantial growth over years and surprisingly all of their subsidaries brands are doing quite well over years which is evident to their leadership capability.

Their stock has increased 200 euros (150 euros to 350 euros)over 3 years and now they have a market capitalization of $176 billion. Within a mild level of debt of $11 billions with $8.5 billions in annual cash flow, 77% of the company’s debt is well covered by its cash flow.

The CEO of LVMH Bernard Arnault has been driving LVMH to success for over 30 years and has no sign of retiring anytime sooner. The company has demonstrated a state-of-the-art leadership and management skills within all these subsidiaries and the executions of embracing innovation and assuring public influence.

Overall, LVMH is operating extremely healthy with substantial growth opportunities. By positioning itself as the leader of the industry and expanding itself geographically in Asia, we can see LVMH would be able to generate more loyalty and popularity in the future.

Future

In the future, LVMH will have to address three of the biggest problems ahead.

- Louis Vuitton’s brand desirability might be threatened by too much exposure in the current market

Louis Vuitton has taken over 40% of LVMH net sales and LV itself stands as the powerhouse of the entire luxurious fashion industry. In the past years, the economy has shown a stagnated state of growth and Louis Vuitton has shown in average 8% growth in net sales over the past 5 years. It is definitely a great sign but it has revealed one of its potential danger as the luxurious giant where the ubiquitous presence might decrease LV’s luxurious social recognition.

Maintaining supply and demand is far easier to be said then done. Now Louis Vuitton has to prepare itself to encounter for this risk. Adjusting the future price up might stimulate second-hand trades and decrease future demand where decreasing the lifetime of its products like what Apple did just seemed far unethical/impossible. One way Louis Vuitton is implementing now is doing collaborations with high tier street brand and possible sports brands where they had crossover with Supreme and Off-White etc.

The increasing volumes of products within the ecosystem is an unavoidable problem and the key strategy of the company is to keep inventing new products with distinct features and freshness. This is yet to be the biggest challenge within the design retail industry and specifically the luxurious ones.

2. Geographical expansion to China might be not as prospect as we think

The Chinese consumers have taken over 20% of the Louis Vuitton net sales, in 2019 they have recorded an unheard growth of 16% in the Asia area, but the breakthrough to Asian might not be as easy as it seems.

Firstly, the China-US trade relationship stands a big factor within the Chinese spending habits. If the trade war has ended with an unpleasant result, the Chinese would its anti-US spendings habits where the refuse to buy iPhone is one of the best examples of it. Secondly, LV is only a portion of LVMH, its susidaries brands like Sephorma and Christian Dior have found it difficult to enter this giant Chinese market. China’s prominent players within the Markets like Alibaba would lead to companies like Sephorma that has less exclusivity facing a tough direct competitions.

3. Counterfeit problems remain unsolved in most countries

Counterfeiting is a specific legal term to describe crime and often most countries have a bad execution on counterfeiting goods. In 2015 the International Chamber of Commerce reported that the global economic and social impacts of counterfeiting and piracy reached $1.7 trillion and this needs be to address in terms of protecting Louis Vuitton brand desirability and its consumers who bought the real products.

As technology arises most luxurious brands might found a way to encounter these goods. By implementing blockchain technology where each products manufactured would be assigned and coded with a unique code (just like a block), whenever transaction of its ownerships occurs, buyers would code their name within the blockchain system and it ultimately takes record of the lifetime of each transaction and assures it is real.

If you have a different thought towards the article or if you want to know more about certain topics I mentioned above? Feel free to contact me (alex.ha4121@gmail.com)! Thanks for your support!